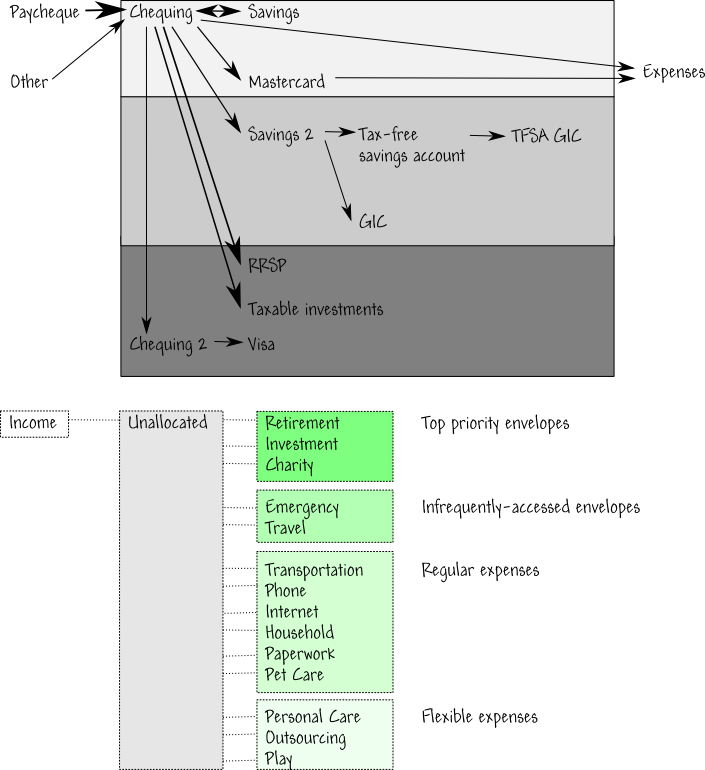

So, about this influence map thing:

(click for a bigger version)

I’ve written about introspection and goals. Now to write about personal finance and planning!

I enjoy learning about personal finance. I love balancing my books, evaluating my spending, and even doing my taxes. I’ve set up my retirement investments and a good opportunity fund. I live a simple, frugal, and abundant life.

What I like about personal finance isn’t just the dollars and cents of it, although I do enjoy working with numbers. I like the way decisions help me understand and clarify my values. Is that really worth spending on? What do I want to save up for? What would make my life better? How can I use money and/or time (they’re very closely related) to make other people’s lives better?

How did I get to this point?

Relatives: I learned a lot about personal finance from our relatives on both sides of the family. People had different kinds of luck. Sometimes they struggled with finances, and they turned to my mom for help and advice. Sometimes they did well, and I saw how perseverance helped them make the most of opportunities. Sometimes, they were blindsided by sickness or accidents, and I learned that I needed to prepare.

I learned from the stories my mom and dad told me about growing up in very different circumstances. For example, my mom told us how she used to walk back and forth in front of one family’s house hoping to be invited in for lunch, and how her mother used to make and mend her dresses until the fabric fell apart. My parents told us stories about starting their business with PHP 1,000 and a borrowed camera, and how they built it from the ground up. I liked how they saw money as a tool to create or pursue opportunities, not as an end in itself, and I learned a lot from that.

House: Another story my mom told me was about how she and my dad bought the house which eventually grew into the studio. It was the worst of times – martial law and the assassination of Ninoy Aquino—but my mom and dad realized that they still liked the Philippines more than anywhere else. So while real estate was at the bottom, my parents scraped together enough money to buy the property they had been renting. I remember my mom telling me how she avoided debt as much as possible, using savings and reinvested profits to grow.

This reminds me of another story my parents like to tell, and which my mom has shared on her blog:

There were two entrepreneurs, one Filipino and one Chinese. They both had a “sari-sari” store (a humble variety store that sells, in retail, only small low-priced everyday items).

After a year, the Filipino used the profits of his store to buy himself a TV set. The Chinese man reinvests his money into the store, and turned his “sari-sari” store into a mini-grocery.

After the second year, the Filipino bought himself a second-hand car while the Chinese continued to commute using public transportation. He expanded his store, while the Filipino still had the same “sari-sari” store.

After the third year, the Filipino bought himself a house in BF Homes (a medium-level suburban subdivision) while the Chinaman continued to live in a tiny room above his store, which was by then, close to looking like a department store.

At this point, my husband butted in and said, “You see, the Chinese way is better,” to which I replied, “Better for the business but look at the two and see who is smiling.” It was easy for the three of us to reach the conclusion that the Chinese knew how to do business, while the Filipino knew how to enjoy life.

“Let’s have a Chinese decision,” John said. “Let’s offer to buy this house. After all, the studio is here, we won’t need to transfer, we might lose clients if we transferred, we won’t have to change business forms and stationary, etc.”

“Okay”, I said, “for now, we will have a Chinese decision, but I hope someday, we can enjoy a Filipino decision.”

The Chinese Decision, Harvey Chua

This taught me about the power of reinvesting and the value of enjoying the rewards.

Passbook: I remember my mom opening a savings account for me and showing me the regular deposits in a small passbook. I didn’t do much with it, but I remember realizing that you can have money even if it’s not in your wallet, and it’s great when it grows without much work.

Potlatch: I remember reading (in Childcraft, of course – loved that series!) about a Native American custom called the potlatch, where people demonstrate their status by giving away or burning (!) expensive goods. I liked the part about providing for others and how it all balanced out, but I wasn’t sure how burning goods made sense. Some cultures value frugality, too, and they provide an interesting contrast.

Monopoly: Our childhood games of Monopoly shaped my drive towards financial independence.

My mom occasionally tells a story about how we played Monopoly when my sisters and I were growing up. In the game, my eldest sister often gave my parents investing advice, my middle sister kept giving her money away, and my parents would often end up giving me money. With a seven-year difference between me and my eldest sister, I suspect that the finer points of real estate value, probability, and negotation were lost on me, and my parents probably just wanted to help me stay in the game. (Saling pusa.)

My mom probably sees the story as a wonderful example that three children can have very different temperaments. For me, that story’s one of the reasons why I think about money a lot. I plan and save so that I can enjoy financial independence. I find it difficult to accept gifts that feel extravagant, because I don’t want to be the spoiled youngest child. I keep my life simple and live within my means.

It also showed me that although luck can change the situation a little bit, once there’s a bit of an advantage, it’s easier to succeed if you’re successful and harder if you aren’t.

Parents: I learned a lot from my parents’ decisions, and I also learned from their partnership. My dad’s more of an generous and impulsive spender, while my mom is the one who budgets, saves, invests, and keeps records. It works well for them, and they’ve figured out how to avoid the control conflicts that often challenge other couples with different spending styles. My dad has come to enjoy Suze Orman’s show (particularly the part about whether people can afford something or not), and he’s even made jokes about it, like whether he could afford to buy a La-Z-Boy recliner for my mom. (“Mr. Chua, go buy your wife a La-Z-Boy!”)

Books: I learned a ton about personal finance from books, of course. I devoured all the personal finance books my mom had, and even today, I enjoy reading things I pick up from the library. Most of the personal finance books cover the same basics and I’m happy to keep my finances boring (index funds, etc.), but sometimes I come across interesting insights. Blogs and forums are great for ideas, too. Books give you the “bones” of a good strategy, while blogs and forums are good for figuring out more about what you want and what’s worth spending on.

My favourite personal finance book is “Your Money or Your Life'”, which has a particularly clear explanation of how to evaluate your expenses and calculate how much of your life you’re swapping for the things you have.

I also remember reading Virginia Woolf’s essay, “A Room of Your Own”. It talked about the freedom you can have by having your own money and a space where you won’t be disturbed. I remember thinking: I love what I do, but I’d still like to save up enough money so that I can freely do what I want to do.

I like what another personal finance book suggested: preparing a bare-bones plan, a comfortable plan, and a realistic plan. The bare-bones plan gives you confidence and a safety net, the comfortable or luxurious plan teaches you about what you value, and the realistic plan helps you enjoy some of that luxury without going overboard.

School: I liked math in grade school and high school, although calculus and I had a bit of a fight in university. Because math didn’t scare me, dealing with numbers in my personal life was okay, too.

I remember how my parents used to help us with math by translating exercises into real-life situations. That helped me learn, and it also showed me that math is useful.

Another story from school: my mom told me about how they were surprised by a bill from the school canteen. Apparently, my middle sister had negotiated her own line of credit with the canteen staff and had forgotten to tell my mom. She used it to not only buy extra snacks, but occasionally treat her classmates. I learned that negotiation skills are awesome, but surprises might not necessarily be so.

Credit card: My mom was always very firm on this. Credit cards are useful, but never carry a balance on them. I never have. She also taught me about keeping enough in my checking account to be safe from overdraft fees, and never buying anything unless I have the money to pay for it. I remember realizing that even though my parents signed for things, they didn’t get them for free, and they earned the money by working hard.

Travel: I learned a lot from how my parents saved up for and planned our big trips. We stayed in youth hostels instead of hotels, ate sandwiches instead of eating in restaurants, and walked or took public transit instead of taking cabs. This meant that we could enjoy more days on our vacation, and we had a more local experience, too. I learned that you don’t have to spend a lot in order to have a great time. I also learned a lot from the way my sister saved up for her trip to South Africa. Normally more of an impulsive spender, she became very careful with her spending. I remember how she shared with us that she was about to buy a hamburger, but then she realized that if she didn’t buy the hamburger, she could enjoy one more meal in South Africa. =) She also told us stories about how she backpacked and lived frugally while in South Africa, making the money last as long as she could. I learned that a clear and vivid goal can really help you examine your spending decisions, and that decisions have opportunity costs.

Immersion: In university, we all went on immersion programs, spending a few days living among the poor. Some of my classmates lived in the countryside. My group lived among the urban poor in one of the city slums. Many of my groupmates couldn’t take it, trying to soften the experience by bringing lots of canned goods or taking a breather by escaping to a nearby mall. Aside from being a little self-conscious about my accent and the attention we drew, I was fine with staying there and sharing people’s lives, eating rice and sardines with my hands, showering with a dipper, and learning how to prepare the food that they sold in mobile street carts.

I remember thinking about how my classmates were shocked (shocked!) once they stepped outside our lives of relative privilege. I remember listening to my host mother’s wry reflections that some families work hard to get out of the muck and some families drink and gamble themselves into oblivion or destruction. I remember the parish priest talking about how there were just so many children, and my host mother saying, ah, well, what can people do? I remember walking past shanties with shiny DVD players and karaoke machines, thinking about the story my parents told about the Chinese entrepreneur and the Filipino entrepreneur. I remember how some people were happy and some people were angry and some people were sad, and it was just like all the rest of the world.

Opportunity fund: When I was in second year, my team and I won a programming competition that had a top prize of PHP 1M, or roughly USD 20,000. Split five ways, it was still a decent sum and more money than I had ever had. I was on a scholarship and didn’t need the money, so my mom saved it for me.

In my final year of university, I wanted to explore wearable computing for my final-year project. The head-mounted display was pretty expensive for an experiment (USD 750 at the time, I think), and I wasn’t sure if it would be worth it. I realized it would be useful to think of my programming competition winnings as an opportunity fund for experiments. I ordered the head-mounted display, and I got tons of mileage out of that. Not only did I learn a lot about hacking, Emacs, wearable computing, and the interaction of society and technology, but I stumbled into the public imagination and I learned how to deal with television interviews, magazine features, and so on. Mass media had covered some of our programming contests in the past and one tabloid had featured me as a computer prodigy at the tender age of five or something like that, but the Borg-like contraption was something else entirely. Even as I protested that I’d shifted from head-mounted displays (too heavy, too obvious, too distracting for people) to speech synthesis (much more interesting, with applications for accessibility), people fixated on the cool stuff. I was made up (as in eyeshadow!), celebrated, misquoted, misspelled (often – my name is hard! ;) ), misrepresented (I hadn’t invented the thing, despite what Seventeen Philippines printed)… and yet, looking back, it was a good thing to do. It was good to be able to take some of that money, create that opportunity, learn something new, and nudge people’s imaginations. I learned that an opportunity fund and the freedom to experiment can lead to all sorts of good things, and that it takes very little to get something going.

I used this idea in Japan, too. Taking advantage of the decent stipend that the Association for Overseas Technical Scholarship gave us during our internships, I took weekend trips using cheap overnight buses to get to Osaka, Kyoto, and Kobe. I took public transit to places like Hakone, and I went to onsens to enjoy the hot springs. I explored different places in Tokyo and surrounding areas, too, like Akihabara (of course!). I think that of all my classmates, I probably had the best time. Again, it helped to set aside some money in my budget so that I could explore without worry.

Canada: Moving to Canada made me grow up. I managed my money carefully as a student. My funding covered tuition and a decent stipend, which I stretched by cooking for myself and keeping my lifestyle simple. I tracked all of my expenses and reviewed my budget regularly. I finished my master’s with no student debt and decent savings.

Using an insight from one of the productivity books I’d read, I listed my goals and ideas, and I started figuring out the price tags for them. I realized, for example, that having a good set of plates and cups and bowls meant something to be, that Corelle was well within my budget, and that tea parties or dinner parties were definitely doable.

When I started working, I kept my student lifestyle, eating at home and borrowing books from the library. I took advantage of the registered retirement savings plan program to defer taxes on my investments. I started building up an even bigger opportunity fund and a decent emergency fund, too. I tried the free financial counseling at work, but the advisor and I figured out that it wouldn’t work out for us, as I had figured most of the stuff out and I liked my low-MER index funds more than actively managed high-MER funds.

W- is also pretty frugal, although I update my books more regularly than he does. We often talk ourselves out of watching movies or eating out because we enjoy the alternatives. We’re both good at saving up for major expenses and keeping a buffer for emergencies. We both enjoy the little things in life, but aren’t afraid to spend where it counts. I’m glad we both care about financial responsibility. That reduces the risk of money causing tension. If many couples fight over money and we can figure out how to keep money from putting us under pressure, we’ll be better prepared for great adventures.

What have I learned about personal finance and planning?

- Money is a means to an end. You can use it to create experiences or explore opportunities.

- Goals and experiments can be surprisingly affordable. Plan, prioritize, and figure out the price.

- There’s a difference between needing something and wanting something.

- Be careful with your financial commitments. Don’t commit to more than you can handle.

- Invest for the long term. Don’t be scared by volatility, but don’t try to be too fancy.

- Don’t beat yourself up with buyer’s remorse. Learn from your decision and move on.

- Contribute to your favourite charitable causes. It helps you make a bigger difference than you could on your own.

- Build in room for “play money” in your budget, and use that to treat yourself and others. If you forget, you might end up feeling deprived, which throws your willpower out of whack.

- Build in room for “dream/opportunity money” in your budget. Use that for key opportunities and experiences.

- It really helps if your partner and you are both frugal, but even if you have different spending styles, you can make things work if you work together.

- The library is awesome. Tax dollars hard at work.

- A little planning today can lead to lots of awesomeness tomorrow, twenty years from now, and so on.